Little did I know how soon I'd be back to report on the status of the last line of my most recent post - specifically my declared hope/dream to be rid of the SVXY that became like a pebble in my shoe.

Yesterday (July 20th), when VIX scraped low in the elevens and SPX scaled a steep hill, I starting thinking about and fearing a future that might not include SVXY prices more attractive than those I was seeing point-blank. Biting the bullet and sweating through the pain, I sold all shares of SVXY and then bought back all shares of TVIX, enjoying for the second the sensation of a clean plate, a fresh slate, and freedom from a position I had not been happy with since taking it on more than a month ago.

Then I turned attention to the fragment still left after cleaning up, the element making the plate NOT clean at all. Perhaps as a balm to the recently acquired wounds (SVXY is what I speak of; not referring to the TVIX which never did a thing to harm me) I decided to leave my SVXY short calls (had previously been covered) undisturbed. (Now naked.) So all I could hope for was one direction for VIX and the other direction for its friend SVXY, and I'd call SVXY a friend as I'd reap (hopefully) the benefit from deflating premium on the calls I had sold (detailed in previous post). Those calls were SVXY July29 61.50 calls, sold for $1.00 last Friday, July 15th. Pictorial of the story is below:

Oops! I gave away the ending to this story. Today in a fit of fear that SVXY might rise again to bite me (no, more like rip my leg off), I made the decision - loathe though I am to ever take a loss - to buy those calls back for $1.10 each. Two reasons went into the decision: 1. I didn't want to wait and see if this option would move against me even more than it already had. Yesterday it traded for $1.60, and that was with SVXY never reaching so high as $61 during the day. Significant moves higher in SVXY next week would inflict some real damage on me, I knew. So I took the not-quite-even buying price and got out. 2. While I wanted to stick to my original plan and just have the shares called away from me next week and keep the premium, I had already negated half that plan (I had sold the shares), and after accounting for the risk I just mentioned in point 1, I didn't think waiting one week to learn the outcome of this trade was worthwhile or prudent. In making the calls naked, I had turned the nice dog on a leash into a Tasmanian devil off the leash.

So that's all scrapped and I'm not very happy about it. Let's total up all the gains and losses in the pile, though, to assess the exact damages:

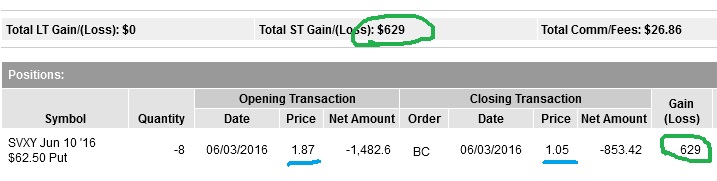

As printed last week:

Above is one small collection of trades revolving around the SVXY position. There is the $1,867 collected as short put premium; this resulted in the shares being put to me (you will see below that some were put to me early and some upon expiration.) Also, there are two sets of covered calls I wrote against the shares after they were put to me; one set expired worthless and I booked $307 gain; one I bought back and booked $173 gain.

Add in the remainder of the transactions:

There are the lots of shares put to me; 600 shares assigned to me on Tuesday of the week of expiration and 200 shares assigned after expiration. Then you see my sale of the shares today. The difference is my loss on the shares. Also above are the calls I wrote against the shares last Friday; today I bought them back at a loss of $107. Not pictured is a fee I had credited to me by the brokerage as a courtesy, which the kids suggested be used to buy ice cream (and that we did.)

Adding the pluses and subtracting the minuses goes like this: Pluses: $1,867 + $173 + $307 + $20 + $48,230 = $50,597. Subtract: -$39,020 -$13,020 -$107 and the end result is a minus figure of $1,550.

Let's not forget to mention TVIX shares sold short and then covered. I mentioned in the last post that I had sold TVIX short at $1.60.

Yesterday (July 20th) I covered them at $1.37 and will look for a place to re-short. See the first graphic in this post. As of this writing (Thursday, July 21st at 2:40PM), TVIX is $1.45. What is it as you read this post? With the help of VIX, which I doubt will stay the same every minute from here on out, I'll make sure we have plenty to talk about next time - you can be sure of that!