She sells short shares down by the SVXY shore... Or something like that goes the nursery rhyme. But does she buy calls to go with those shares? Probably not. Here's why I did it:

I wanted a chance to benefit from the SVXY downside I envisioned without worrying excessively about the potential penalty for being significantly unfortunate in my timing/prediction. So, feeling confident that my dream of SVXY put through the macerator would come true, I decided on a price I'd be willing to pay (which would also cap my loss), should my dream waft away in the mist of a sunny mid-September morning.

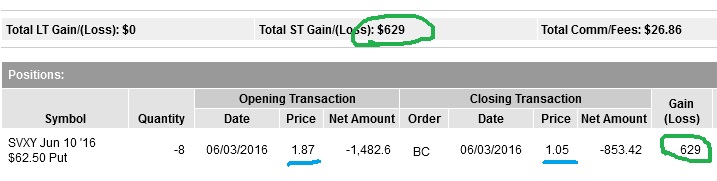

I looked around for a call I could buy that would guarantee me the right to cover my short shares at a specified price. SVXY was trading near $74 at the time, but the only near-to-price contracts available right then for my desired expiration were at the $75 and $70 strikes. I decided to pay for the three of the $70 calls, knowing that about half the price was intrinsic (I'd make it back cent-for-cent upon buying my short shares back for a profit) and the other half was time premium. Then I sold a corresponding number of shares short at the going price which was under 74 at the time. A few days later I added on another long call and the appropriate number of shares at prices that didn't differ much from the initial position (see second image for individual prices), but improved (raised) the break-even point by a smidgen. I settled down to wait and watch with my 400 short shares and four long calls. I now had an average entry point of 73.77 in the short shares and an average cost of $6.75 for the long calls. The outcome at expiration would look like this: (Three paragraphs will explain three basic outcomes)

Look at the diagonal line above the yellow-blocked area. It starts at my break-even point, which would be SVXY trading at 67.02 at expiration. Any SVXY price below 67.02 would represent a profit of better than 6.75 per share on my SVXY short entered at 73.77. This equates to $2,700+ in profit since I had sold 400 shares short. The maximum I could lose on the calls would occur if none of the $2,700 I had spent were able to be recouped (and every last cent would be expected to drain out of the calls if SVXY were to close anywhere below 70), so every cent lower than the 67.02 break-even would increase my profit upon closing the short (setting a $2,700 options loss against a greater-than $2,700 share gain), thus the diagonal line going upward in ever-increasing profit projections.

See the yellow-blocked area. At one end is SVXY at 70; at the other end is SVXY at my break-even of 67.02. Remember, I purchased for myself the privilege of closing my short shares for a price no higher than 70. So, SVXY trading at any price higher than 70 would not adversely affect me past my worst-case scenario; I'd be out for my maximum loss no matter how the share price might climb, and if SVXY sunk below 67.02 I'd make increasing profits as described above. But anywhere in between those prices would represent a loss (at expiration) less severe than the maximum, based on a combination of two factors: The expected total loss in value of the calls as they expire under the strike price set against a profit realized by closing the short for some price less than 70.00 but greater than 67.02.

All this is off the table if I would choose to close the trade before expiration. Anytime before that, some value would likely remain in the calls, depending on the interaction between the time remaining until expiration and the moneyness (just made up that term, if it doesn't exist already). Obviously I anticipated that SVXY might end up anywhere over the strike or instead sink, slither, sneak, descend in an orderly manner or outright plummet below 70 to points so far within the basement you can't hear an answer back when calling to it. You can tell which one I was hoping for. My plan was to gladly hand over the $2,700 for the opportunity to run free through the ruins of SVXY during the future-vision fantasy world (that might never unfold for me) in which volatility would spike so high that SVXY would get destroyed and reduced to ashes and embers. Here's what actually happened:

Look at the orange arrow in the above chart, which shows where I closed this position. Then see on the chart how the rest of the trading day unfolded. By the end of Friday, SVXY was back to 71.45 and those calls traded at 4.32. How would I have fared, just sitting around watching and then closing this at the end of the day? For shares shorted at 73.77 and closed at 71.45, and calls bought for 6.75 and sold for 4.32, it would net out to a "now you see it, now you don't" profit, and in fact, a little bit of loss. Good thing I struck while the iron was hot. The iron's even colder now, with SVXY currently trading (as of this writing on Monday, August 29th in the afternoon) at 72.99 and the calls trading for 5.16. I'd be looking at something like a $300 loss to get out of the position, were I trying to close it right now.

Moving on to the next trade, which I'll be sure to document here, but not before I know what it's going to be! Some ideas are already in place, of course, but I have to watch and see what happens, just like all of us are doing. Until next time... And - Careful trading!